All Categories

Featured

Table of Contents

The inquirer stands for a client that was a complainant in a personal injury issue that the inquirer worked out on part of this complainant. The defendants insurance firm accepted pay the complainant $500,000 in a structured negotiation that requires it to purchase an annuity on which the plaintiff will be detailed as the payee.

The life insurance business releasing the annuity is an accredited life insurance coverage business in New York State. N.Y. Ins. an annuity may best be defined as. Legislation 7702 (McKinney 2002) states in the pertinent part that" [t] he purpose of this post is to supply funds to safeguard resident. beneficiaries, annuitants, payees and assignees of.

annuity agreements,. released by life insurance policy business, based on particular constraints, versus failure in the efficiency of contractual obligations because of the disability of insolvency of the insurance company providing such. agreements." N.Y. Ins. Legislation 7703 (McKinney 2002) states in the relevant part that" [t] his article will apply to.

N.Y. Ins. The Department has reasoned that an annuitant is the holder of the basic right approved under an annuity agreement and stated that ". NY General Advice Point Of View 5-1-96; NY General Guidance Point Of View 6-2-95.

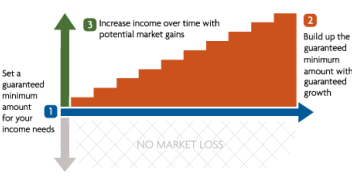

How Does Retirement Annuity Work

Although the owner of the annuity is a Massachusetts firm, the designated recipient and payee is a citizen of New york city State. Since the above specified objective of Post 77, which is to be liberally interpreted, is to protect payees of annuity contracts, the payee would certainly be shielded by The Life insurance policy Company Warranty Company of New York City.

* An immediate annuity will not have an accumulation phase. Variable annuities provided by Protective Life Insurance Coverage Business (PLICO) Nashville, TN, in all states other than New York and in New York City by Protective Life & Annuity Insurer (PLAIC), Birmingham, AL. Securities offered by Investment Distributors, Inc. (IDI). IDI is the principal underwriter for signed up insurance items released by PLICO and PLAICO, its associates.

Definition Of An Annuity Contract

Financiers must very carefully take into consideration the financial investment objectives, threats, fees and expenditures of a variable annuity and the underlying financial investment choices prior to spending. This and various other details is contained in the programs for a variable annuity and its hidden investment options. Prospectuses might be acquired by calling PLICO at 800.265.1545. annuity ins. An indexed annuity is not a financial investment in an index, is not a safety and security or stock market investment and does not join any type of stock or equity financial investments.

The term can be 3 years, five years, 10 years or any number of years in between. A MYGA works by connecting up a swelling sum of money to permit it to collect interest.

Deferred Variable Annuities

If you pick to renew the agreement, the rate of interest rate may differ from the one you had actually originally accepted. An additional option is to transfer the funds right into a different kind of annuity. You can do so without facing a tax obligation fine by utilizing a 1035 exchange. Because interest rates are set by insurance coverage companies that offer annuities, it is necessary to do your research study before signing a contract.

They can defer their taxes while still utilized and not seeking added gross income. Offered the current high rate of interest, MYGA has actually become a significant element of retired life economic preparation - bank annuity rates. With the possibility of rates of interest decreases, the fixed-rate nature of MYGA for a set number of years is highly appealing to my customers

MYGA prices are usually more than CD rates, and they are tax deferred which better enhances their return. An agreement with even more restricting withdrawal provisions might have higher prices. Many annuity carriers offer penalty-free withdrawal provisions that enable you to withdraw several of the cash from an annuity before the abandonment period ends without needing to pay charges.

In my opinion, Claims Paying Capability of the service provider is where you base it. You can look at the state warranty fund if you want to, but bear in mind, the annuity mafia is watching.

They understand that when they put their cash in an annuity of any type, the business is going to back up the case, and the industry is overseeing that. Are annuities guaranteed? Yeah, they are. In my point of view, they're secure, and you must go right into them considering each carrier with confidence.

If I put a recommendation in front of you, I'm also putting my permit on the line. I'm really certain when I placed something in front of you when we talk on the phone. That does not indicate you have to take it.

Companies That Buy Annuities

We have the Claims Paying Capacity of the carrier, the state warranty fund, and my friends, that are unknown, that are circling with the annuity mafia. That's a valid solution of a person who's been doing it for a very, very long time, and who is that a person? Stan The Annuity Man.

Individuals normally get annuities to have a retirement revenue or to develop cost savings for one more function. You can acquire an annuity from a qualified life insurance representative, insurance policy business, monetary coordinator, or broker. You must speak to a financial adviser about your requirements and goals prior to you purchase an annuity.

Fixed Annuity And Variable Annuity

The distinction between the 2 is when annuity payments start. enable you to conserve money for retired life or other factors. You do not need to pay taxes on your earnings, or payments if your annuity is an individual retired life account (INDIVIDUAL RETIREMENT ACCOUNT), until you withdraw the profits. allow you to develop a revenue stream.

Deferred and prompt annuities provide several alternatives you can pick from. The alternatives supply different degrees of potential risk and return: are ensured to earn a minimum interest price.

enable you to pick between sub accounts that resemble mutual funds. You can make much more, but there isn't a guaranteed return. Variable annuities are greater danger since there's a chance you could lose some or all of your cash. Set annuities aren't as risky as variable annuities since the financial investment danger is with the insurance policy business, not you.

Types Of Annuities For Retirement

Set annuities guarantee a minimal rate of interest price, typically in between 1% and 3%. The company might pay a higher rate of interest price than the ensured passion rate.

Index-linked annuities show gains or losses based on returns in indexes. Index-linked annuities are more intricate than fixed deferred annuities.

Each relies upon the index term, which is when the firm calculates the passion and credit ratings it to your annuity. The establishes just how much of the increase in the index will certainly be used to determine the index-linked rate of interest. Various other vital features of indexed annuities include: Some annuities cover the index-linked rates of interest.

The floor is the minimum index-linked passion rate you will earn. Not all annuities have a floor. All taken care of annuities have a minimum surefire worth. Some firms make use of the standard of an index's worth as opposed to the worth of the index on a defined date. The index averaging might take place whenever throughout the regard to the annuity.

The index-linked interest is contributed to your original premium amount yet does not substance during the term. Various other annuities pay substance passion throughout a term. Substance interest is passion gained accurate you conserved and the interest you make. This indicates that interest already attributed additionally earns passion. The passion gained in one term is generally compounded in the following.

Best Single Premium Immediate Annuity

This percent may be made use of as opposed to or along with an engagement price. If you get all your cash before completion of the term, some annuities will not credit the index-linked passion. Some annuities could credit only component of the passion. The percentage vested typically raises as the term nears the end and is always 100% at the end of the term.

This is because you birth the investment threat as opposed to the insurer. Your representative or economic consultant can help you make a decision whether a variable annuity is right for you. The Stocks and Exchange Compensation categorizes variable annuities as safety and securities since the performance is stemmed from stocks, bonds, and various other financial investments.

Individual Annuity

Find out more: Retired life in advance? Think of your insurance coverage. (us life annuity) An annuity agreement has 2 stages: a build-up phase and a payment phase. Your annuity earns rate of interest during the build-up stage. You have numerous alternatives on exactly how you add to an annuity, depending upon the annuity you buy: enable you to pick the time and amount of the settlement.

The Internal Profits Service (IRS) controls the taxation of annuities. If you withdraw your revenues before age 59, you will possibly have to pay a 10% early withdrawal fine in enhancement to the taxes you owe on the passion earned.

After the buildup phase finishes, an annuity enters its payment phase. There are a number of alternatives for obtaining repayments from your annuity: Your business pays you a dealt with amount for the time stated in the agreement.

Lots of annuities bill a charge if you withdraw money before the payout phase. This fine, called an abandonment cost, is usually highest possible in the very early years of the annuity. The charge is commonly a percent of the withdrawn money, and normally starts at around 10% and goes down annually up until the surrender duration mores than.

{kind=link}

Table of Contents

Latest Posts

Understanding Fixed Vs Variable Annuity Pros And Cons A Comprehensive Guide to Fixed Vs Variable Annuity Pros And Cons What Is Fixed Annuity Vs Variable Annuity? Features of Fixed Income Annuity Vs Va

Understanding Financial Strategies A Closer Look at Tax Benefits Of Fixed Vs Variable Annuities Defining Fixed Annuity Vs Equity-linked Variable Annuity Benefits of Choosing the Right Financial Plan W

Highlighting What Is Variable Annuity Vs Fixed Annuity A Closer Look at How Retirement Planning Works Defining the Right Financial Strategy Pros and Cons of Fixed Annuity Vs Equity-linked Variable Ann

More

Latest Posts